In order to close the financing gap in green technologies, finding new mechanisms to enhance the participation of the private sector, combined with that of the public sector, in financing sustainable and climate-resilient infrastructure is a must. In this context, some unlisted instruments are going to be needed to enhance financing of green infrastructure. Besides, the development of properly structured projects, with risks and returns in line with the preferences of the different types of investors and financial agents that make up the ecosystem of financing sources, would also help to close the private financing gap in infrastructure. The Moroccan infrastructure planning framework gives an example of many implementable mechanisms to facilitate the development of sustainable infrastructure.

Challenge

The Programme for Infrastructure Development in Africa (PIDA) report (2012) highlighted the pressing infrastructure needs of African countries, particularly in Sub-Saharan Africa. Sustainable infrastructure in Africa is still today the missing link towards deeper integration of the African continent. The lack of physical and social integration costs the continent 2 per cent in annual growth. For example, at the time the report was issued the energy sector needed around $30 billion in investments per year, in order to match a projected six-fold increase in energy demand by 2040. As things stand today, the first step of the PIDA programme failed to achieve the needed interim objectives. The selection process faced many hurdles but the most important aspect is that the quantity of projects considered under the first phase came at the expense of quality (African Union, 2020). In particular, some projects failed to align with the goals set by the 2063 Agenda of the African Union, and this lack of efficiency in the selection process hindered the full participation of the private sector.

Consequently, there is an urgent need to find new mechanisms to enhance the participation of the private sector in financing sustainable, climate-resilient infrastructure in the African continent, combined with the participation of the public sector. Indeed, according to the latest Global Infrastructure Hub outlook, risks that are contingent to infrastructure projects peak during the construction phase. During that phase, the private sector is very reluctant to engage in a project without the appropriate guarantees. Furthermore, climate risks associated with climate change have both a direct and an indirect impact on the sustainability of existing infrastructure. On the one hand, the probability of fat-tail events (e.g., natural disasters) increases. On the other hand, climate risks can lead to an increase in the total cost of projects including an increase in the share of the capex that accrues to the private sector.

Developing countries’ rising demand for energy has mostly been met with fossil fuels. Today, in order to move forward in their decarbonisation plans and meet the climate agendas, these countries must work on shifting their infrastructure investments to green infrastructure, by developing more low-carbon and climate-resilient infrastructure, especially in the energy field.

Climate-resilient or green infrastructure investments are investment activities focused on projects or areas that are committed towards preservation of the environment such as pollution reduction, fossil fuel reduction, conservation of natural resources, generation of the alternative energy sources, projects related to the cleaning and maintenance of air and water, waste management or any other type of environmentally conscious practice.

Such a shift towards green infrastructure can strongly enhance a structural change in infrastructure investment, and can be a trigger for sound economic development, spurred by green growth. According to the International Energy Agency (IEA), every additional dollar invested today in clean energy can generate three dollars in future fuel savings by 2050 (OECD/IEA, 2012).

In this context, governments have a key role to play in strengthening the enabling environment for green infrastructure investment. By doing so, the public sector will mitigate the risks inherent to investment in infrastructure projects in general and to green ones in particular and allow the private sector to invest in green infrastructure projects. In particular, the private sector can help:

- Avoid the lock-in to carbon-intensive development pathways.

- Reduce fossil-fuel reliance for energy-importing countries.

- Create domestic jobs by including national SMEs in the investment process.

In addition, private sector expertise applied to green energy infrastructure can facilitate cost-effective access to energy in rural and remote areas. Finally, private sector know-how may foster innovation.

Given the current strains on public finances, due to the massive public expenditure engaged to face the COVID-19 crisis, and the considerable infrastructure (and particularly green infrastructure) gaps, achieving this green transition will entail leveraging both international and domestic private financing. Private investment in green infrastructure however remains seriously constrained by some investment barriers, such as high upfront costs, high perceived risks and long investment timelines compared to fossil-fuel-based alternatives.

Our analysis builds on the idea that unlisted instruments are going to be needed to enhance financing of climate-resilient projects. We analyse the role of the public sector in mobilising finance (public and/or private) to facilitate investment in green infrastructure. We organise the analysis around two broad dimensions: i) measures to facilitate financial challenges, and ii) measures to facilitate market regulation/contract design.

Proposal

DIMENSION #1: FINANCIAL MEASURES TO FACILITATE INVESTMENT

As highlighted in the Challenge section, there is an important gap between the needs for investment in infrastructure in a substantial part of the world economy, more particularly in Africa, and the abundance of financial resources in search of investment opportunities with returns greater than those of low-risk assets. While we acknowledge the existence of different explanations for the wedge between needs and investments in African infrastructure, our focus follows the dimension of financing which, in line with G20 priorities, we consider as a major obstacle in the continent.

Although this gap can be observed both across continents and within countries, Africa epitomises the phenomenon. Indeed, with rare exceptions, such as China, investment in infrastructure has remained below what is necessary to expand the countries’ potential growth (Canuto and Liaplina, 2017). While financial resources in world markets are facing low long-term rates of return, opportunities for greater potential returns with infrastructure assets are being lost. The development of properly structured projects, with risks and returns in line with the preferences of the different types of investors and financial agents that make up the ecosystem of financing sources, would help to close the private financing gap in infrastructure.

Investors and financial agents have different mandates and their own competences regarding the management of risks associated with types of projects and phases of investment project cycles. They demand coverage of risks whose exposure is not adequate or permitted by regulation. The absence of complementary instruments or investors is one of the causes most often associated with failure in the financial completion of projects.

Defining attractive investment opportunities for different types of investors and combining these perspectives more systematically around specific projects or sets of assets is a promising way to bridge the infrastructure financing gap. The planned and integrated issuance with different time profiles of fixed income securities, bank loans, credit insurance and other financing structures aimed at the different moments, from the preparation to the operation of projects, makes that combination possible.

Additionally, as observed in multiple consultations with stakeholders, they highlight the relevance of having financeable project pipelines featuring homogeneity, quantity and comparability that stimulate them to create technical analysis capacity and to invest in financial intermediation.

Lately, the interest with respect to infrastructure finance has turned to climate-resilient projects (which we will generically call “green”). They represent a particularly important subset of infrastructure projects, because green projects are unlisted investments which makes data gathering very difficult. In that sense, improving project data disclosure would be helpful for financial institutions. Moreover, regulated requirements on disclosure (transparency) may accelerate the creation of international benchmarks.

Moreover, with the aim of facilitating the creation of a pipeline of projects, clarifying the meaning of “green infrastructure” seems necessary. To that end, a standard taxonomy of green investment needs to be created (as globally as possible). Correspondingly, this taxonomy requires the institutional architecture to define it. When considering Africa’s infrastructure projects, the definition of the above taxonomy requires striking a balance between climate resiliency and social relevance. Indeed, Africa’s pressing infrastructure needs would need to be socially optimal and, when it comes to providing incentives, fiscally feasible. Given the current orientation of the world economy towards the green transition, African countries are seeking to take on the momentum as well by preparing green infrastructure for the future. These should answer a triple objective of safeguarding the climate; creating, stimulating and sharing the prosperity; as well as emancipating individuals and offering an environment conducive to risk-taking.

On the other hand, all of the above measures are oriented fundamentally to facilitating financing of long-term contracts. However, market environments that impose the development of infrastructure under the same framework as traditional projects may create undesired constraints. This challenges the adequacy of a convergence to a pure infrastructure-like market design. In particular, mitigating risk implies that investors are not facing the risk that technology may be replaced (or become obsolete), even if it exists. The counterpart of the long-term contract, which is typically a regulated consumer, absorbs this risk. Furthermore, if the riskier contracts are discouraged, technological flows channelled through utilities will face barriers to be developed (Arbouch, Canuto and Vazquez, 2020).

In summary, interesting lines of action are:

– Risk mitigation instruments must adapt to the financial ecosystem: Financial instruments offered to the private sector may not be adapted to potential consumers (those who aim to lend). For example, offering relatively short-term debentures has, in theory, the logic of structuring investments that enhance the main loan (“base facility”). However, due to the short-term characteristics of the product, the buyer will not (normally) be an institutional investor. Potential buyers, typically banks, would normally prefer a loan, as it is a more liquid instrument.

– Avoid “crowding out”: Any long-term loans from the private sector must compete with public loans. In this sense, there is a risk of creating barriers to entry into the private sector. Note that it is not enough to just reduce the volume of public sector loans (i.e., when the public sector loan runs out, Special Purpose Entities (SPE) would use the most expensive instrument), as the profitability of projects when they enter into concessions is often calculated in relation to this loan. More expensive loans make projects unfeasible.

– Changing the role of public financing: Optimising the role of public financing implies acting on the risks in which the private sector perceives more difficulties. One of the potential objectives would be subordinated debt (in general, “mezzanine” financing): an instrument that absorbs credit loss before senior debt, which increases the quality of that senior debt. In this sense, subordinated debt can be designed with different risk/return rates, constituting a bridge between traditional debt and equity (Vazquez, 2018).

– In relation to “green investment”, relevant measures would be: i) disclosure of climate change risks for infrastructure assets, and ii) standardisation, taxonomy and green definitions. Both objectives are more or less interdependent. Indeed, proper measures and definitions of climate-related risks require the existence of a set of positive nomenclature of green assets and infrastructure as an asset class. Harmonisation helps reduce the overall volatility of the contingent risks and thereby reduces part of the measurable uncertainty faced by private investors.

DIMENSION #2: MARKET DESIGN MEASURES

As noted by Arbouch and Bourhriba (2020) and Hausmann (2018), long-term contracting has been systematically used as a tool to coordinate public and private forces to deliver crucial infrastructure. Traditionally, governments often choose to bear the risks related to the construction phase and some risks related to the operation in order to ensure the full compliance of the private operators. This allows countries with limited fiscal space to build green infrastructure and reduce their funding gap. Moreover, new investments in crucial infrastructure can have strong spillover effects on job creation and the creation of peripheral activities. However, while these mechanisms are particularly useful, they do not come without drawbacks. Perhaps the most important one is the challenge of moral hazard that comes with risk mitigation by the public sector (Mann, 2018). Excessive risk-taking by the private operator sometimes leads to the accumulation of liabilities on the government balance sheet. Another important aspect relates to the contracts per se, which are systematically renegotiated, often to the benefit of the private contractor.

The starting point for a well-designed contract to finance green infrastructure should be the fact that green infrastructure projects are sufficiently similar to other infrastructure projects and should rely on proven project financing approaches. The key difference is that many green infrastructure investments require financial support to mitigate externalities, which private sector stakeholders alone have no ability to afford.

Second, many green infrastructure investments require subsidy support, but this is not different from any other infrastructure project. In many green infrastructure projects blended finance is used, and such schemes are more common as projects become more complex and not viable if relying only on private sector financing.

Finally, a well-designed contract to finance green infrastructure will accelerate investment in green technologies by resolving their financing challenges. As such, the focus should be on obstacles that have impeded the financial closure of green infrastructure investments. Moreover, the successful financial closure of low-emission projects will improve their contribution to climate change mitigation by locking new investments into clean technology over their lifetime, while displacing low-cost polluting alternatives. This is significant as carbon mitigation initiatives often deal with emissions of pre-existing assets rather than introducing new clean investments.

AFRICAN CASE STUDIES

As stressed in the challenges, Africa is today the continent where investment needs in sustainable infrastructure are most pressing. Also, according to the latest projections by the IPCC, it is more exposed to global warming. This calls for a novel approach to finance resilient and sustainable green infrastructure. Previous studies have shown the importance of sound infrastructure in enhancing growth. For example, Agénor et al. (2008) study the link between foreign aid, public investment in infrastructure, growth and poverty. They find that aid, coupled with reforms, has a positive impact on growth and poverty.

The experiences of Morocco and Sub-Saharan Africa shed light on some of the many tools that could be used to enhance private funding of infrastructure and logistics, on the one hand, and the emergence of a market for infrastructure as an asset class where needed, on the other.

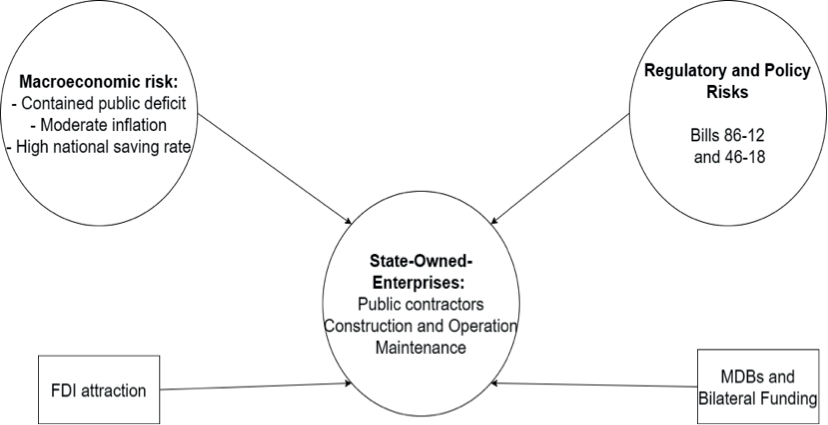

In the Moroccan approach, the public sector plays a central role in introducing the tools to mitigate the risks pertaining to large infrastructure projects, to attract the private sector and acting on multiple fronts. First, the legislative front through incentive-compatible legislation on public-private partnership (PPP) that creates synergies and provides guarantees and readability to the private contractor. Second, the macroeconomic front through a disciplined and well-designed approach to macroeconomic policy which matches the needs of attracting the most needed capital flow, official and private, channelled towards structuring projects. Last, public-driven vehicles of development in the form of state-owned enterprises that drive and support the creation and the application of infrastructure planning, together with private contractors. This is a genuine model that helped the country achieve important steps in improving its infrastructure assets and create the perfect environment for the private sector, especially the banking sector, to participate.

Today, Morocco stands as an emerging model with advanced expertise that can benefit the whole continent to build green resilient infrastructure. According to the latest figures from the infrastructure compass by the Global Infrastructure Hub, Morocco achieves infrastructure scores higher than the average of the upper income countries.

1. Morocco

In light of the recent advances made by Morocco in modernising its infrastructure, this country offers an interesting perspective on how other African countries can rely on the public sector with the participation of the private sector in building sustainable green infrastructure, capitalising on a strong involvement of the government and state-owned enterprises, in special PPP schemes.

First, to ensure the consistency of decisions with the legislative cycles and avoid discretionary changes, the parliament has adopted a framework for PPP implementation through Bill no. 86-12 that was voted in 2014 and amended in 2020 through Bill no. 46-18. Both bills insisted on the importance of PPPs as mechanisms that would help the country achieve long-term goals of sound and sustainable infrastructure that can help achieve social inclusion and improve the quality of the offer of public services. Also, the initial bill came with a standardised definition of a PPP contract with its different clauses, while the amendment bill cleared the way for private sector participation in structural projects, with significant social returns. Both emphasised the importance of transparency in the process of procurement and the importance of information disclosure.

Second, throughout the last two decades, and with the exception of cyclical events, Morocco has kept a sound macroeconomic framework, based on strong fundamentals and a moderate but sustained growth rate. This helped the country improve its overall business climate and its attraction of foreign direct investment in crucial areas like renewable energy, port infrastructure or the new industrial zones, giving the much needed visibility to the private investors to correctly assess the returns of infrastructure projects. For example, between 2014 and 2018, the statistics of the foreign exchange office of Morocco show a twofold increase of the total stock of investment in the Energy and Extraction sector.

The last ingredient of the Moroccan model, and perhaps the most fundamental, is its reliance on state-owned enterprises that are the main operators of infrastructure in the country (e.g., Autoroutes du Maroc, Tanger Med, etc.). State-owned enterprises (SOEs) sign the contracts on behalf of the government which, in theory, should ensure the sustainability of the long-term relationship between the private and the public contractors and prevent political and bureaucratic interference in the operational decisions. The state as the main (only) shareholder acts as an underwriter for its enterprises, providing guarantees to the private partners. In practice, problems of coordination and suboptimal governance of some of these SOEs prevail. This has led the country to reform the governance of public enterprises through the creation of the Mohammed VI fund and the new agency of state participation, which will be in charge of transforming public enterprises. One particular expected advance is the integration of the infrastructure operated by these entities in their balance sheet as a proper asset.

Figure 1. The Moroccan Model of Infrastructure Development, authors

Thanks to this model, Morocco has been able throughout the last two decades to strengthen its infrastructure assets and enlarge the coverage in basic infrastructure such as roads, water and electricity to a large share of the population. Three specific programmes have been fundamental in that course.

First, Le Programme d’Electrification Rurale Globale has enabled the country to enlarge its coverage of electricity in the rural areas. The programme was run and partly financed by the National Office for Electricity, with multilateral as well as private funding, based on a collaborative approach with rural households. A major component of that programme was its reliance on renewable energy technologies, through a pilot phase then a generalisation through a fee-for-service scheme that opened the way to private provision.

Second, Programme d’Approvisionnement Groupé en Eau potable des populations Rurales, which enabled access to drinking water, was run and financed by the National Office for Drinking Water, another public entity, in partnership with the local communities, the beneficiaries as well as concessional loans from multilateral development banks (MDBs). This programme has helped more than double the access to drinking water in rural areas throughout the last two decades. It also had indirect effects on the overall enrolment in basic education for rural children.

Finally, the Programme Nationale des Routes Rurales, launched in 1995, has helped expand the network of rural roads. The coverage of rural roads went from 54 per cent in 2005 to 80 per cent in 2017. This project was piloted by the Moroccan Ministry for Equipment and Transportation, and financed by MDBs, especially the World Bank. A survey held by the latter institution showed that the project helped increase girls’ access to basic education by 7.4 per cent.

2. Sub-Saharan Africa

Private participation in infrastructure investment is hampered by the poor quality of local legal and regulatory environments, weak project preparation capacity and underdeveloped or untested PPP arrangements. These challenges are compounded by weaknesses in institutional and funding arrangements, including for the setting up of special purpose vehicles, the process of issuance of project bonds, and arranging private placements and syndications, all of which would normally be precursors to or accompany the process of issuing listed securities.

As we observe in many jurisdictions over the world, long-term finance for infrastructure is largely dependent on unlisted products. As we pointed out in the general analysis, one of the main challenges for the creation of more organised markets providing long-term funding is the lack of more standardised projects. This likely limits the development of deeper markets for corporate finance, thus making larger developers face the need to rely on the banking system, which normally has a strong preference for short-term contracts for infrastructure investment.

Several reforms in Sub-Saharan Africa (SSA) countries have created growing private pension systems (Della Croce, Fuchs and Witte, 2016, p. 143). For instance, “the Nigerian pension industry grew from USD 7 billion in 2008 to USD 25 billion in 2013; total assets under management in 10 African countries in 2015 reached close to USD 380 billion, with South African pension funds managing a commanding share of 85% of these assets (USD 322 billion)”.

These institutional investors, on the other hand, represent a small fraction of project funding. An alternative could be to consider domestic capital markets in SSA. There are some emerging hubs, such as Nairobi and Lagos (ibid.), but short-term liquidity is still limited.

The most developed capital market in the African continent is that of South Africa, which is characterised by a growing base of institutional investors. In this regard, an interesting example of using fixed income capital markets to finance infrastructure projects is that of the South African “Touwsrivier Solar Project”. A green bond was issued in the local currency with a face value of ZAR 1 billion, to finance the construction of a 44 MWp concentrated photovoltaic plant in an economically impoverished part of the country.

In that view, except South Africa, the depth of equity markets in SSA is relatively low in terms of capitalisation and liquidity of equity markets. In that context, we observe that funding of infrastructure projects largely relies on government funding, donors and foreign direct investment.

CONCLUDING REMARKS

We may identify two elementary business models associated with green investment: i) the “utility business model” is based on a firm that undertakes long-term investments and recovers them by selling the output through oneto two-year contracts; ii) the “infrastructure business model” is based on selling the output of an infrastructure through long-term contracts.

Financial structures in the two types of business model are considerably different.

We may summarise the requirements of each model succinctly: short-term contracting requires liquid capital markets, whereas long-term contracting requires planning. Although there are no silver bullets, the market design needs to be coherent in order to attract private investment for green infrastructure projects. Hence, measures to facilitate them will differ depending on the requirements of the green infrastructure considered.

The challenge today is how to take the collaboration of the private and the public sectors to the next step. In other words, how can we assess and mitigate the risks that are inherent to green infrastructure projects? The proposed path for green financing would look like this:

– In order to avoid the crowding-out effect, one may revisit the strategy “the public sector takes care of long-term financing, the private sector takes the short term”. An alternative strategy may be: “Eliminate barriers to entry for the private sector”.

– How to do that? One of the most used designs to facilitate financing of green projects is combining a long-term contract that hedges the project’s income stream with a public vehicle to provide relatively cheap (compared to market prices) long-term debt.

– Public financing might be optimised, in the case of green infrastructure, by focusing on absorbing riskier investments. For instance, public instruments may play the role of bridging traditional debt and equity.

REFERENCES

African Union, NEPAD (2012), Study on Programme for Infrastructure Development in Africa (PIDA)

African Union (2020), L’Approche du Corridor Intégré – « Un cadre holistique de planification de l’infrastructure pour établir le PIDA-PAP 2 »

Agénor, Pierre-Richard; Nihal Bayraktar; and Karim El Aynaoui (2008), “Roads out of Poverty? Assessing the Links between Aid, Public Investment, Growth, and Poverty Reduction”, in Journal of Development Economics, Vol. 86, No. 2 (June), pp. 277-295

Arbouch, M.; and O. Bourhriba (2020), “African Infrastructure Development: What Should Be Done to Win the Next Decade?”, in Globsec Policy Institute

Arbouch, M.; O. Canuto; and M. Vazquez (2020), “Africa’s Infrastructure Finance”, in Policy Briefs for the T20’s TF3: Infrastructure Investment and Financing

Canuto, O.; and A. Liaplina (2017), “Matchmaking Finance and Infrastructure”, in Policy Center for the New South Policy Briefs, No. 23, Rabat

Della Croce, R.; M. Fuchs; and M. Witte (2016), “Long-Term Financing in Sub-Saharan Africa”, in Banking in Sub-Saharan Africa Recent Trends and Digital Financial Inclusion, p.143

Hausmann, R. (2018), “The PPP Concerto”, in Project Syndicate, 30 April

Mann, H. (2018), “The High Cost of “De-Risking” Infrastructure Finance”, in Project Syndicate, 26 December

OECD/IEA (2012), Energy Technology Perspectives: Pathways to a Clean Energy System

Vazquez, M. (2018), “Financing the Transition to Renewable Energy in the European Union, Latin America and the Caribbean”, in Florence School of Regulation Policy Briefs, No. 12